Why Registry Records Override Facts: Transaction Risks of Undischarged Encumbrances

- The Dictatorship of the Registry: Public Faith vs. Material Truth

- Institutional Filters: Why Notaries and Banks Block Transactions

- Anatomy of the “Registration Gap”: A Comparative European Timeline

- Scenario Analysis: Mortgages vs. Court Seizures

- Risk Matrix: What Happens in the “Priority Window”

- Navigation Strategies: How to Transact Safely

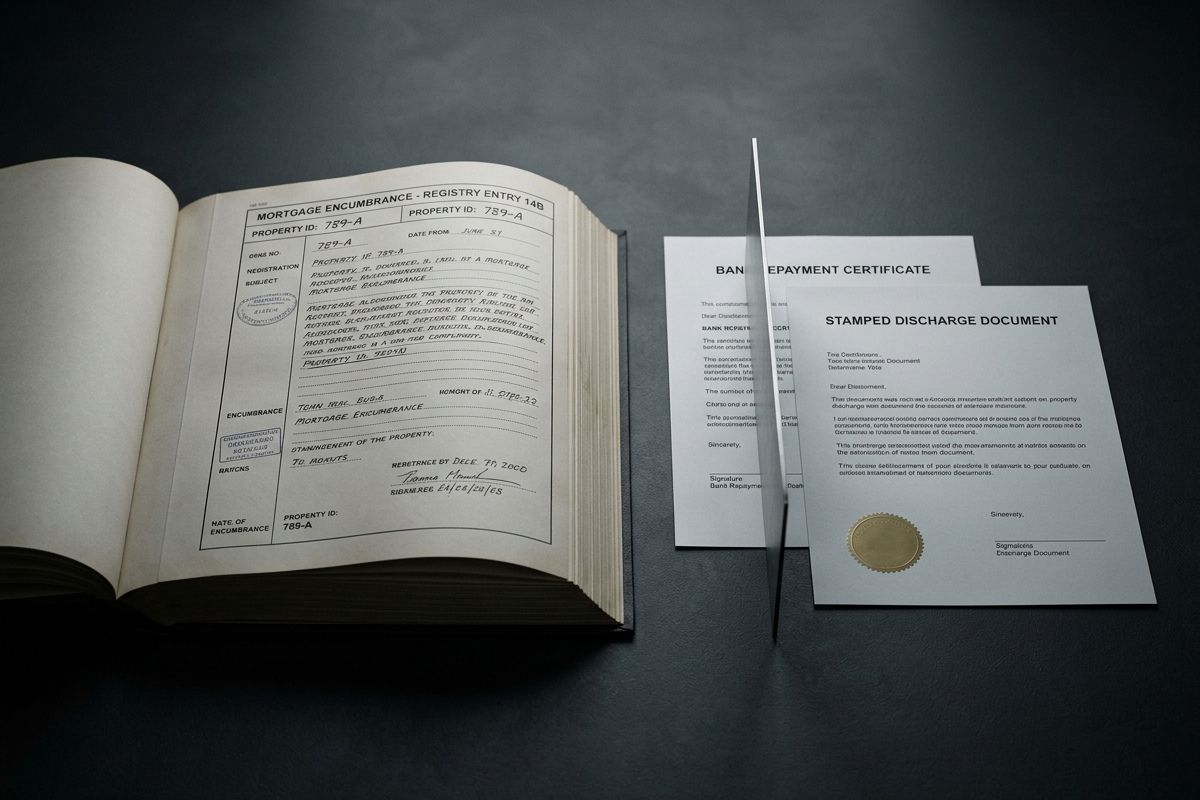

For most participants in the real estate market, a bank certificate confirming full loan repayment or a final court order lifting a seizure seems like the finish line for clearing a title. However, in European legal systems based on the principle of the public faith of the register, legal reality does not align with the facts until the registrar physically modifies the database. This creates a “registration gap”—a dangerous period during which the property remains formally encumbered, turning any transaction into a zone of institutional conflict.

This article explains why the formal persistence of a registry record suppresses private evidence of the discharge of an obligation, creating a systemic barrier that forces market participants to use specialized protective mechanisms—from priority notices to notarial escrows—to manage priority risks.

How do European legal systems resolve the institutional conflict between a substantively terminated obligation and its persistent registration during the “registration gap”?

Scope of Analysis

A comparative analytical review of the legal systems of Poland, Germany, the Czech Republic, Spain, and the UK in the context of managing mortgage encumbrances and court seizures.

Key Legal Principles

- Public Faith of the Register (Publica Fides): the presumption that the content of the register is correct for any bona fide third party.

- Priority Principle (Prior Tempore): the order of rights is determined by the time of their entry into the register, not the moment the obligation arose.

- Continuity of Title (Tractus Successivus): the requirement for a consistent chain of records to perform any registration act.

Key Legal Terms

- Registration Gap: the time interval between filing an application and the actual entry being made in the register.

- Constitutive Registration: a record that does not merely record, but creates or terminates a right (e.g., a mortgage in Germany).

- Priority Notice (Vormerkung): a mechanism for reserving a place in the queue of rights to protect the purchaser.

The Dictatorship of the Registry: Public Faith vs. Material Truth

In Civil Law systems, the land registry is not merely an archive but an active market regulator. The principle of public faith (Öffentlicher Glaube or Rękojmia wiary publicznej) is designed to protect the stability of transactions: a buyer must trust the book rather than verify suitcases full of receipts. However, this same principle turns against the owner when an obligation is terminated but the record remains.

An entry in a state register possesses legal autonomy: it continues to generate legal consequences for third parties even after the substantive grounds for its existence have ceased to exist.

The legal irony is that if a buyer sees a debt discharge certificate, yet the register still contains a mortgage record, they may lose their status as a “good faith purchaser.” Courts in Poland and Germany often interpret knowledge of a discrepancy between the register and the facts as “gross negligence,” stripping the buyer of the protection the register was supposed to provide. Thus, the existence of a fact does not grant immunity from the dictatorship of form.

Institutional Filters: Why Notaries and Banks Block Transactions

This table reveals why professional market participants refuse to recognize out-of-court evidence of title cleanliness.

| Institution | Verification Focus | Reason for Blocking | Unblocking Condition |

|---|---|---|---|

| Notary | Current encumbrance section | Risk of liability for entering a “dirty” title into the system | Final court order or notarized bank consent for discharge |

| Lending Bank | Priority of rights in the register | A new bank’s mortgage cannot take first rank while the old one remains | Physical expungement of the record or a formal “promesa” from the predecessor |

| Registrar | Formal compliance of documents | Principle of Tractus Successivus requires closing the old branch first | Flawless application (Antrag) with the original discharge consent |

Anatomy of the “Registration Gap”: A Comparative European Timeline

The duration of the period during which a transaction remains in “limbo” varies radically depending on the administrative efficiency of the system. While timelines in the Czech Republic are strictly regulated, the registration gap in Poland can reach critical levels, turning a purchase into a lottery.

Comparative analysis shows how different jurisdictions manage the technical lag in updating registries.

| Jurisdiction | Average Discharge Term | Legal Effect of Discharge | Priority Protection Mechanism |

|---|---|---|---|

| Germany | 2–4 weeks | Constitutive | Vormerkung (Priority Notice)1 |

| Poland | 3–10 months2 | Declarative (primarily) | Ostrzeżenie (Warning) in the register |

| Czechia | 30 days | Constitutive | Plomba (Entry pending notice) |

| Spain | 15–30 days | Constitutive | Asiento de presentación |

| UK | from 1 day | Administrative | Overreaching (clearing interests with capital) |

2 In major Polish cities (Warsaw, Kraków), the processing times of the Land and Mortgage Courts (EKW) remains the most problematic node in the analyzed system.

Scenario Analysis: Mortgages vs. Court Seizures

The type of encumbrance determines the parties’ strategy. Discharging a bank mortgage is a predictable commercial process, whereas lifting a court seizure carries a high risk of administrative failure.

Risk Matrix: What Happens in the “Priority Window”

The main danger is not the old record itself, but that it blocks the “sterility” of the register needed to protect a new transaction. Until the register is updated, any new record filed in this interval enters a struggle for priority.

Analyzing cascade risks allows for an assessment of the real cost of waiting for a registry update.

| Risk Type | Trigger Mechanism | Probability | Consequences |

|---|---|---|---|

| Loss of Priority | A new creditor files a seizure while the old one is being “discharged” | Medium | The transaction is invalidated or the property is re-encumbered |

| Procedural Block | An error in the bank’s documents is discovered by the registrar 3 months later | High | Transaction deadline failure; buyer’s loss of deposit |

| Funding Refusal | Bank compliance does not accept certificates as a substitute for a registry entry | High | Transaction collapse due to lack of funds |

Navigation Strategies: How to Transact Safely

The choice of protective instrument depends on the parties’ risk appetite and the specifics of the jurisdiction.

| Registry Situation | Protective Instrument | Legal Effect | Security Level |

|---|---|---|---|

| Mortgage discharged (DE/CZ) | Vormerkung / Plomba | Guarantees that no entry made after the transaction will be valid | Maximum |

| Seizure lifted (PL/ES) | Notarial Escrow | Funds are transferred to the seller only after a “clean” extract is issued | High (Financial) |

| Complex Dispute (EU) | Escrow Account | Full control of payment conditions by an independent agent | High |

| Any “Phantom” Record | Title Insurance | The insurance company assumes the risk of a title defect | Medium |

In modern European land registration systems, “title cleanliness” is an administrative state rather than a factual one. The central risk of a transaction involving undischarged encumbrances lies not in the old obligation itself—which has already been fulfilled—but in the loss of “good faith” protection due to the buyer’s conscious disregard of the “polluted” state of the register. A safe strategy requires a move away from trusting “certificates” in favor of strict priority-fixing mechanisms or withholding payment until the physical cleaning of the register is confirmed.

- Regulation (EU) No 1215/2012 — European Union

- Act on Land and Mortgage Registers — Poland

- Ley Hipotecaria — Spain

- Cadastral Act (Katastrální zákon) — Czech Republic

- Land Registration Act 2002 — United Kingdom

- Civil Code (BGB) — Germany

Похожие записи:

Court Decision Not Reflected in Land Registry: Systemic Gap

Court Decision Not Reflected in Land Registry: Systemic Gap

Can You Sell an Apartment in Ukraine While Wanted Under TCC: The Truth About “Oberih” Registry and Notarial Checks

Can You Sell an Apartment in Ukraine While Wanted Under TCC: The Truth About “Oberih” Registry and Notarial Checks

Why a Court Decision Does Not Change the Land Registry Record

Why a Court Decision Does Not Change the Land Registry Record

“Silent Arrest”: How a 17,000 UAH TCC Fine Can Derail a Property Sale in Ukraine

“Silent Arrest”: How a 17,000 UAH TCC Fine Can Derail a Property Sale in Ukraine

“Reserve+” Collision: Notary Refusal in Transactions Using Foreign Power of Attorney in 2026

“Reserve+” Collision: Notary Refusal in Transactions Using Foreign Power of Attorney in 2026

Request a Callback